Understanding the retirement calculators

# This post was inspired by the Fun With Numbers post over at BigGuyMoney.com

There’s a big problem in the UK, the US and most other developed countries around the world; People are not saving enough for their retirements. Speaking to friends and colleagues on the subject, it’s clear most of them can be split into two different camps:

Vastly underestimating their required savings

These are the people who believe that putting in their minimum workplace scheme contributions for 40 years will eventually yield a pension worth a large percentage of their current salary.

Greatly overestimating their required pension

Those who believe that they will need over a million pounds to be able to retire and are unable to stop working until this is reached.

Although these groupings can appear to be at opposite ends of the spectrum to each-other, the cause always comes down to misinformation or misinterpretation of the information given through mainstream media and government policy.

“I contribute to my pension every month, what’s the problem?”

The UK government is in the process of implementing a compulsory workplace pension scheme for nearly all employers in the country. This aims to ensure that the majority of employees in the country are contributing 8% (4% self, 3% employer and 1% government topup) into a workplace pension scheme. The problem with this, and its something rarely touched upon by either the government documentation or main stream media is that 8% simply isnt enough.

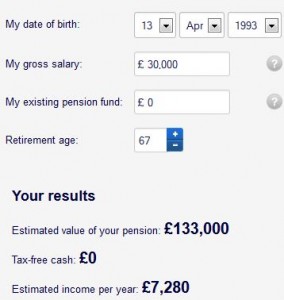

Taking an example of a 21year old male, fresh out of his over-priced university degree and working an average £30,000 job whilst making the required minimum pension contributions:

Combined with a state pension of around £5,800 (If such a thing still exists in 40+ years) and our fresh faced graduate can look forward to a pension of £13,080. Not exactly poverty but likely to be a huge lifestyle change for someone who was previously living on 96% of their salary.The problem is often compounded as salary increases through career progression however contributions remain level. And this is where many of those who setup the minimum contributions and then forget about them are going to find themselves come retirement age.

While government minimum levels are a great starting point and can be used to force the issue of retirement savings upon new employees; it runs the risk of many assuming this is the only level of savings they require and that the rest of their income is free to be spent on consumer rubbish.

“I used a pension calculator, it said I needed £1,000,000 to retire!”

Here we have an opposite but equal problem with many of the retirement calculators offered to the market. Wild assumptions about required income levels during retirement lead to a vastly over-estimated pension pot requirement which then seems impossible to achieve.

I’ve seen mainstream media articles claim you need anywhere from 66% – 100% of your final salary to survive in retirement! Granted; If you intend on traveling the world on non-stop cruises or buying a luxury car every couple of years than your retirement incomes will be higher.. however it’s not unreasonable to assume most retirees will have paid off their mortgage and no longer have dependent children.

The real danger here is that people see these suggested required levels, put them into a retirement calculator which then (correctly) calculates that they need to begin saving a huge percentage of their income for the next 40+ years to achieve it. People become disillusioned and instead decide to forget the whole saving for retirement idea and splash the cash now while they have it – “I’ve no chance of reaching that amount so may as well just spend all my money now”

The real to understanding pension calculators and correctly identifying the income levels they suggest is to take a close look at the assumptions they make. If you’re currently saving/investing (Stocks, mortgage, pensions etc) 50% of your salary it doesn’t make much sense to assume you’d need a huge amount more than that to happily retire on. Similarly; If you’re only saving 4% and living off of the other 96%; you haven’t much chance of reaching that income level in retirement and so will be forced to adjust your lifestyle drastically downwards.

Have you come across some ridiculous retirement income requirements? Please leave a comment below and let me know.

4 thoughts on “Understanding the retirement calculators”

Great information. Keeping expenses low and saving much are the two keys. When most of your “spending” is saving, then you are on the right track.

We have progressed (slowly) through some stages..accumulating debt, paying off debt, saving some, saving 40-50%. I am looking forward to two additional stages. Saving far less (pre-retirement) and Saving none (retirement).

Keeping spending low in the latter stages will be key. If nothing else a retirement calculator can give you some big goal to hit.

Great work on working through your debt and onto an awesome savings rate! I agree, they do give something to aim for.. you just need to be careful that you dont blindly follow them into thinking you’d need far more/less then you actually will.

Great post. I became debt free about 5 years ago, but only seriously started saving/investing earlier this year – better late than never! My target is to save on average 50% of my net salary – so far, I’ve averaged around 40%, so I’m getting there!

I have a friend who’s in her early 40s – somehow she’s got it into her head (and I can’t persuade her otherwise) that pensions are rubbish and so she’s never joined the company schemes that have been available. She says her pension will be the “equity in her house” but surely in order to get to that equity, she’ll have to either sell the house (and then find somewhere else to live) or remortgage when she retires? I just hope she has savings anyway.

Definitely better late than never! 40% of net salary is still pretty awesome and way way above the national averages.

Not joining a company pension scheme is totally nuts. If the company matches contributions (as most do up to a certain level) thats a 100% increase! I doubt you’ll find anywhere else to instantly double your money. Trying to use your house at your pension is a massive risk as you pointed out.. the only way to release the equity would be to downsize massively. Do you really want the stress and hassle of moving when you’re 70? Plus there’s no way a bank is going to remortgage for someone that old. Too many people bury their heads in the sand and end up having to throw themselves at the mercy of state welfare.

Comments are closed.